The Challenge

Active traders and quantitative investors have a data problem: market data streams in faster than any human can process it, from multiple exchanges simultaneously, and a single bad data point can corrupt an entire analysis. The client needed a platform that could ingest high-frequency OHLCV and order book data from multiple exchanges at once, run machine learning pattern recognition across that data in near-real-time, and surface the results through interactive charts — all with sub-second latency. There was zero tolerance for data inaccuracies because actual trading decisions would be made based on what the platform surfaced. Existing solutions either had the data or the analysis, but not both in a single interface.

Our Solution

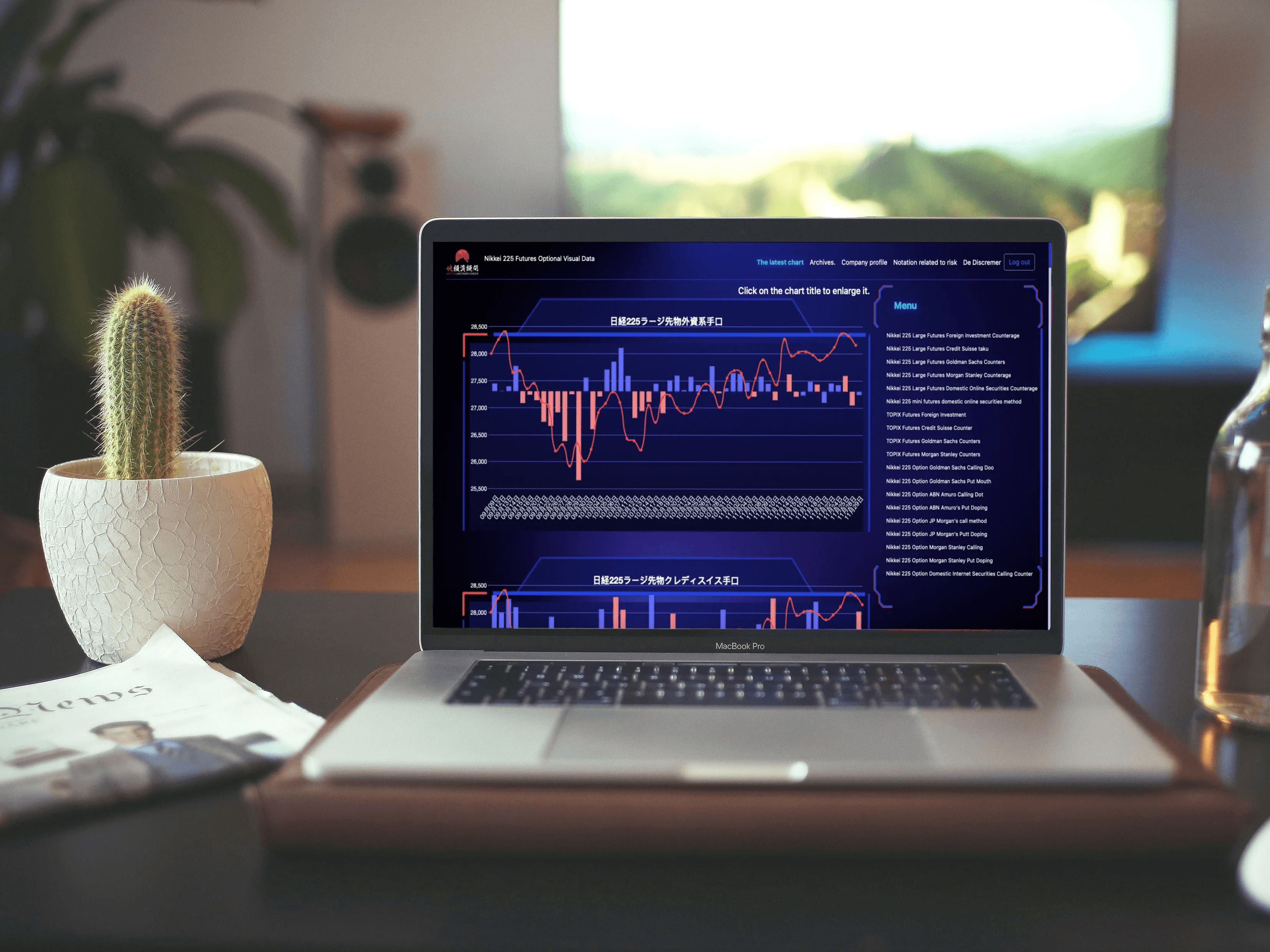

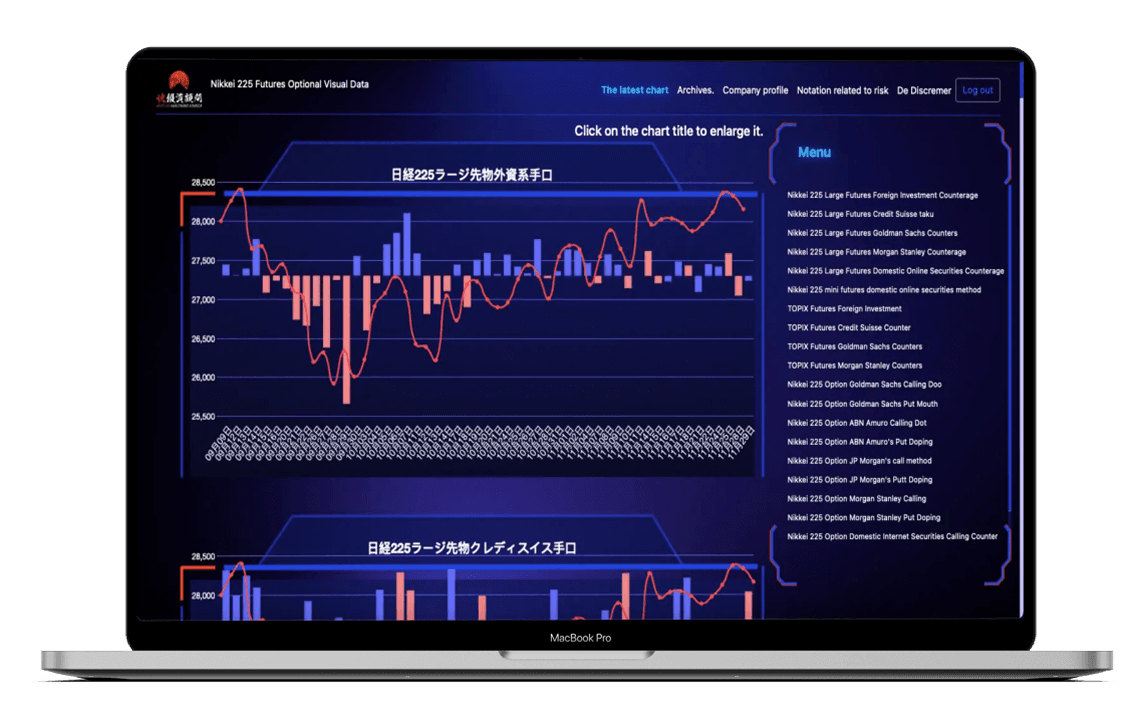

We designed a high-performance market analytics platform with a Python and Django backend built specifically for data pipeline throughput. Market data is ingested from multiple exchange APIs simultaneously and pushed to a Redis in-memory cache, achieving sub-second latency for live price and volume updates. WebSockets stream that live data to a React frontend without polling. The ML layer runs pattern recognition models against both historical data in PostgreSQL and the live Redis feed — flagging potential setups and surfacing them as overlays on the charting interface. Interactive chart components support multi-timeframe and multi-instrument views with custom indicator overlays. The backend is stateless and scales horizontally — as data volume grows, additional processing instances are added without re-architecting the core system.

Key Results

- Processes over 1 million data points per day across multiple exchanges simultaneously

- Sub-second data ingestion latency achieved via WebSocket streaming and Redis caching

- ML pattern recognition surfaces high-probability trading setups directly in the chart interface

- Multi-timeframe and multi-instrument interactive charting with custom indicator support

- Horizontally scalable architecture — data volume grows without re-engineering

- Zero tolerance for data inaccuracies met via validation layer before ML processing

Engineered With

Aesthetics & Function

What Was Delivered

Want to build something like this?

We deliver enterprise-grade software at fixed pricing, in 4–8 weeks. Book a free strategy call and get a no-commitment estimate.

Free Strategic Audit Included